[ad_1]

Asian plastic makers have been eagerly anticipating a post-lockdown pick-up in Chinese language consumption, however weak client demand and excessive inventories imply it might be a very long time coming.

Petrochemicals has been the toughest hit section of the oil market this 12 months. Covid-19 restrictions in manufacturing large China decimated demand over April and Could, whereas the invasion of Ukraine upended gasoline flows and raised prices for naphtha, a serious feedstock.

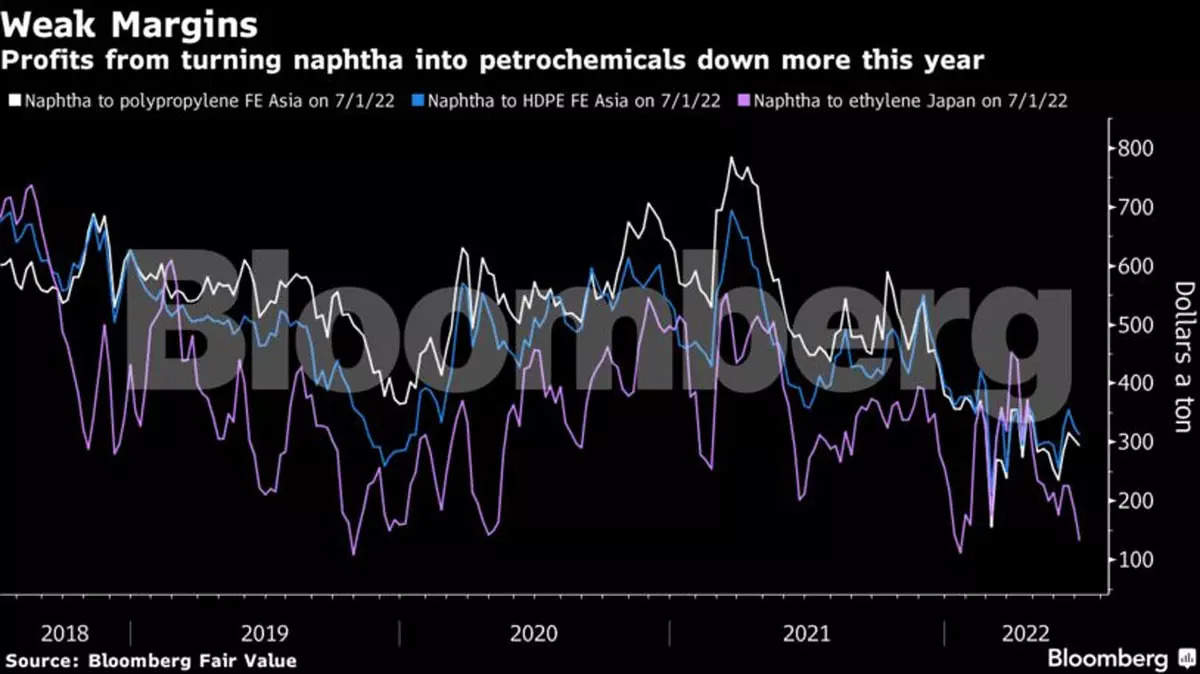

Producers of the constructing blocks used to make the whole lot from automotive interiors to packaging and cables have seen margins fall additional this 12 months. Income from turning naphtha into ethylene, a petrochemical that’s the bottom for a lot of plastic merchandise, have dropped to $133 a ton from above $450 in early April.

“Sturdy plastics for home white items and for automotive purposes have but to see a powerful demand restoration,” stated Larry Tan, vice chairman for chemical consulting in Asia at S&P World. Inflationary pressures in China are “inflicting customers to be extra cautious on spending on bigger-ticket gadgets,” though home sentiment is slowly bettering, he stated.

Larger transport prices and disruptions to produce chains are additionally complicating the worldwide plastics commerce, making it more durable for Asian producers to offset sluggish native demand by exporting to Europe.

Chinese language petrochemical crops have elevated working charges over the previous few weeks, however they’re nonetheless solely working at 85% of capability, in contrast with 100% usually, in keeping with Kelly Cui, a advisor at Wooden Mackenzie Ltd. Stockpiles are additionally excessive, she stated.

There are some optimistic indicators for plastics producers, nonetheless. Benchmark North Asian naphtha costs have fallen by round 30% since spiking in early March after the Russian invasion of Ukraine, though are nonetheless excessive on a historic foundation. A few of their merchandise — corresponding to xylene, toluene, benzene and MTBE — that may be blended with gasoline are additionally seeing sturdy demand.

And Chinese language family spending must also begin to enhance. Goldman Sachs Group Inc. sees it growing 4.5% within the second half from a 12 months earlier, in contrast with a 1.5% contraction final quarter.

Nonetheless, Beijing’s Covid Zero coverage means the danger of extra lockdowns hasn’t gone away, stated Wooden Mackenzie’s Cui. Consumption is slowly on the mend, nevertheless it may take till September, normally the peak-demand interval for polyolefins — a key petrochemical section — to see a firmer turnaround, she stated.

[ad_2]

Source link

{kind=link}