[ad_1]

It’s by no means actually a bear market till all of the stragglers get taken out and shot. So it was only a matter of time earlier than vitality shares, the massive winners for a lot of the primary half of this yr, received nailed.

Now the Vitality Choose Sector SPDR Fund

XLE,

and the SPDR S&P Oil & Fuel Exploration & Manufacturing

XOP,

exchange-traded funds (ETFs) are down 27% to 36% from their 2022 peaks – official bear-market territory.

This is a chance for anybody who missed the vitality rally. The explanation: Unfounded fears are driving the declines.

“Extra to come back? We don’t assume so,” says Ben Prepare dinner, an oil and gasoline sector knowledgeable who manages the Hennessy Vitality Transition Fund

HNRIX,

and the Hennessy Midstream Fund

HMSFX,

Prepare dinner and I had been final bullish on vitality collectively in November 2021. After just a little volatility and sideways motion, XLE and XOP went on to achieve 52% to 58% in eight months.

Now three elements recommend one other robust transfer forward for vitality names, believes Prepare dinner: respectable underlying fundamentals, good valuations and stable money flows. Goldman Sachs predicts large-cap vitality shares will acquire 30% or extra by way of the tip of the yr and that its buy-rated shares might be up 40% or extra.

Simply bear in mind, nobody can ever name the exact backside available in the market or a gaggle. This isn’t a bet-the-farm-for-instant-riches form of name.

Right here’s a better look.

1. Favorable fundamentals

U.S. exploration and manufacturing shares have fallen a lot that they’re pricing in expectations of $50 to $60 a barrel for West Texas Intermediate

CL.1,

says Prepare dinner, down from round $100 now. “We expect equities are pricing are extra dire scenario than is at the moment mirrored in market fundamentals,” he provides.

Certainly, the 2023 futures curve for WTI suggests $88 a barrel oil subsequent yr.

Costs for future supply are notoriously fickle. However this oil value “forecast” of $88 for WTI is consistent with Goldman Sachs “mid-cycle” oil value forecasts of $85 for WTI and $90 for Brent. It additionally is sensible for the next causes.

Provide is constrained. That’s as a result of oil firms have been underinvesting in exploration and manufacturing improvement. This helps clarify why inventories at the moment are meaningfully under historic seasonal norms.

“With little or no provide cushion out there, any additional disruption to produced volumes, both geopolitical or storm-related, may ship pricing meaningfully larger,” says Prepare dinner.

Extra: U.S. oil has tumbled — What that claims about recession fears and tight crude provides

Plus: U.S. crude-oil stockpiles possible declined in newest Vitality Division knowledge, analysts say

Demand will dangle in there. The looming prospects of recession have hit the vitality group arduous. However this can be a false concern. Whereas a recession would decrease demand within the U.S. and Europe, demand will develop in China because it continues to carry COVID lockdown restrictions.

In addition to, recession is just not even essentially within the playing cards. “Whereas the percentages of a recession are certainly rising, it’s untimely for the oil market to be succumbing to such issues,” says Damien Courvalin, the top of vitality analysis and senior commodity strategist at Goldman Sachs. “We imagine this transfer[ in energy-sector stocks] has overshot.”

The worldwide financial system remains to be rising, and oil demand is rising even sooner due to reopening in Asia and the resumption in worldwide journey, he notes.

“We keep a base case view {that a} recession will likely be averted,” says Ruhani Aggarwal of the J.P. Morgan international commodities analysis group. The financial institution places the percentages of recession over the following 12 months at 36%.

Russian oil continues to circulate. Regardless of well-founded outrage over Russia’s invasion of Ukraine, the European Union hasn’t been actually efficient at preserving Russian provide off the market. Europe nonetheless buys Russian oil, and any shortfall in demand there will likely be offset by shopping for in China and India.

Europe’s newest plan is to set value caps to restrict monetary beneficial properties by Russia. It’s not clear how this may work out. However it may backfire. In a worst-case state of affairs, Russia retaliates and cuts manufacturing sufficient to ship oil to $190 a barrel, writes Natasha Kaneva of the J.P. Morgan international commodities analysis group. “Russia had already confirmed its willingness to withhold provides of pure gasoline to EU nations that refused to fulfill cost calls for,” says Kaneva.

2. Valuations

As measured by enterprise worth to anticipated money flows, the vitality group is the most affordable sector on the market now, says Hennessy’s Prepare dinner.

3. Free money circulate

U.S. vitality firms proceed to return lots of money to shareholders through dividends and buybacks, notes Prepare dinner. This may help inventory costs.

The free money circulate yield (money circulate divided by share value ) for the vitality firms within the S&P 500 is larger than that of some other S&P sector. Based mostly on consensus analyst estimates for 2022, U.S. vitality firms will generate a 15% free cashflow yield, and exploration and manufacturing firms will generate a 20% free cashflow yield, says Prepare dinner.

These numbers affirm the cheapness of the group.

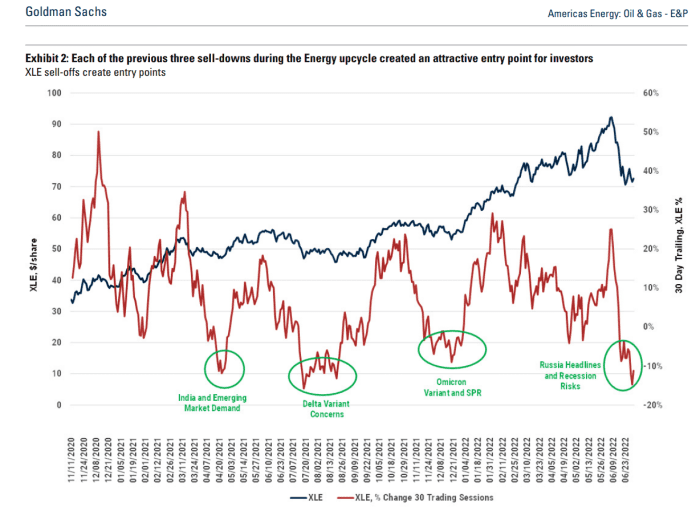

This chart from Goldman Sachs exhibits that every one comparable selloffs in recent times have been shopping for alternatives, given these underlying bullish elements.

Goldman Sachs

Favored firms

Prepare dinner singles out these three firms as favorites.

Exxon Mobil

A blue-chip vitality identify, Exxon Mobil

XOM,

has a diversified enterprise mannequin that dampens inventory volatility, says Prepare dinner. It’s a producer, so vitality value beneficial properties help the inventory.

However it additionally has a petrochemicals division that makes petroleum-based supplies like polyethylene utilized in plastic merchandise like meals containers. This enterprise can offset the adverse influence from weak spot in vitality costs.

It additionally has a liquid pure gasoline enterprise that exports LNG from the U.S. This division advantages from the sharp spike in LNG costs in Europe and Asia linked to Russian pure gasoline provide disruptions.

EOG Sources

This U.S. vitality producer

EOG,

has a few of the highest high quality shale basins within the nation, says Prepare dinner. This offers EOG a price benefit over friends, and it helps robust money circulate. EOG additionally has an excellent observe report of delivering productiveness beneficial properties in wells, and price cuts.

Cheniere Vitality

Like Exxon, this Louisiana-based firm

LNG,

exports LNG to Europe and Asia. So it, too, advantages from the dramatic pure gasoline and LNG value hikes there relative to pure gasoline costs within the U.S. Within the background, Cheniere is paying down its debt, which ought to enable Cheniere to spice up its dividend over the following eighteen months, believes Prepare dinner.

Dividend payers

Goldman favors vitality firms that pay excessive dividends and have low beta shares, that means their shares are extra secure and transfer round lower than the sector or the general market. On this group, Goldman’s favourite is Pioneer Pure Sources

PXD,

Goldman likes the corporate’s big stock of undeveloped property within the Permian basin, and the robust steadiness sheet and free money circulate supporting the stable 7.8% dividend yield.

Goldman has a 12-month value goal of $266 on the inventory.

Michael Brush is a columnist for MarketWatch. On the time of publication, he had no positions in any shares talked about on this column. Brush has urged XOM and LNG in his inventory e-newsletter, Brush Up on Shares. Comply with him on Twitter @mbrushstocks.

[ad_2]

Source link